Why is property cheaper in the US?

Why is property cheaper in the US?

There's one thing they have that we don't...and shouldn't.

It seems high real estate prices are the cause of everyone’s problems, except owners of course!

But when we compare real estate prices in Australia with that of the United States, everyone gets a little anxious.

Who’s heard of the friend that bought a run-down home in some sunbelt state for next to nothing?

Who hears people in Government and the real estate industry talk about ‘build-to-rent’ (developers building to own and rent out, rather than sell) as a solution to the ‘housing crisis’, look at the US, then look back here and lament why the returns aren’t enough to make it viable?

They say comparison is the thief of joy.

I reckon there’s good reason to believe that when comparing Aussie house prices with US ones. There are a few reasons, but there’s one underlying cause, which I will explain below.

Why compare to the US?

The United States is the world’s most advanced market. It is ahead in many things, backward in others, but the sophistication of its capital markets is unmatched. Because it is such a large, advanced economy with deep capital markets, you can find all sorts of listed companies on the New York Stock Exchange. Including listed real estate companies, covering so many niche sectors.

Among these property companies are apartment and home landlords. That’s right. There are companies in the US that own up to 100,000 apartments each, and their job is simply to manage and grow the portfolio. The other beauty of listed companies is the treasure trove of data and information for us to analyse and compare.

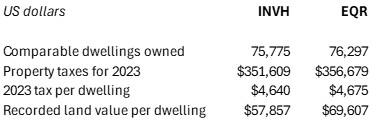

I look at two US companies in particular. The first is Invitation Homes (INVH), a US-listed homeowner of 85,000 homes across the US. The second is recently renamed Equity Apartments (EQR), also listed, which owns around 85,000 apartments across the US. Each company discloses lots of data.

We can see from INVH and EQR financial reports how much they buy, develop and sell dwellings for.

INVH develop for about US$380,000 per home. EQR slightly more, per apartment.

Even if you convert this to Australian dollars (A$584,000), that’s pretty cheap, right?

Yes, but there’s a big difference between buying there and buying here.

The first is lending structure.

Borrowers can ‘walk away from their home’

Australians will be familiar with the “guarantor” (i.e. Bank of Mum & Dad), which means they will be ‘on the hook’ for the mortgage if the borrower defaults. While the home purchased is the security behind the mortgage, the lender can go after the guarantor’s assets (Mum & Dad’s home) if the loan is under water.

While the bank wants to ensure you can afford your mortgage, what it really cares about is the value of your property. This is why the guarantor is needed. Not to service your mortgage if you can’t, but to offer additional property if the value of yours falls below what you owe. The guarantor and lenders mortgage insurance (LMI) only apply with high loan-to-value ratios. If property prices decline, Aussie banks will be in major strife. The whole system is based on rising house prices.

Ergo the US, which is notorious for “non-recourse” lending. This means the mortgage is only secured by the property borrowed against.

If the value of the property falls below what is owing on it, the borrower can ‘hand back the keys’ to the bank. The borrower walks away with nothing (but a bad credit score), and the bank is left with the home. If the home is worth less than what’s owing, it means the borrower is better off.

This is what happened in the fallout of the GFC, as the US housing market crashed and lots of homes had ‘negative equity’. There’s a great paper about how non-recourse lending impacts property prices. The long and short of it — non-recourse lending means more volatile property prices.

However, the main reason why property prices in the US are much lower than Australia’s is simply because the land is so much cheaper over there.

Why is that? Does the US have more habitable and desirable land than Australia?

The short answer is yes, owing to its many cities and better (albeit older) infrastructure. If you have flown into a major US airport and driven on the Interstate, you will understand. If you drive to Brisbane on the New England Highway, you will also angrily understand.

But the core reason US property prices are cheaper?

Property taxes — the real damaging wealth tax

As with most things, real estate is priced relative to the cost to produce it. That is, the cost to develop land and buildings.

For housing, a big component of end value is the land.

How is land priced? Supply and demand, yes, but land is valued using a technique called “discounted cash flow” or “net present value”.

Basically, adding all future expected cash flows from the asset into today’s dollars.

Impact on values

To demonstrate why property taxes explain most of the difference between Australian and US property values, I’ll compare the purchase of a vacant block of land, with no income, and mostly taxes as outgoings.

In Australia, the first big (and antiquated) tax is stamp duty. Depending on the state you live in and any concessions you are entitled to, it could be around 4.5% of the transaction value, borne by the buyer. After the property is purchased, you could be up for land tax, but for the purposes of this analysis I will only include council rates, which no land owner can escape.

Compare this to the United States. They don’t pay rates or stamp duty, but they pay something worse – property taxes. These taxes are levied annually and are paid to the local county.

How bad are property taxes in the US?

We know from INVH and EQR financial reports how much each pay in taxes for how many dwellings owned. The summary is below.

At $4,640 per year per home, Invitation Homes’ average property taxes are nearly 3 times as much as council rates in Australia.

But how do we compare stamp duty, council rates and property taxes?

By calculating a net present value of the taxes paid. See below:

Take a $900,000 block of land in Sydney.

I assume $500 per quarter ($2,000 a year) of rates for a standard suburban block in Sydney.

I also assume property prices in both Australia and the US increase by 5% a year.

After deducting stamp duty and council rates, the Sydney block of land would return 4.6% a year, on average, after deducting stamp duty and council rates. If stamp duty didn’t exist, it would be 4.7%. This means that stamp duty has a negligible impact on returns over 30 years.

Now let’s take what we expect is a $3.9 million piece of vacant land in 2054 (which we purchased today for $900,000) and convert it to US dollars. For a similar block of land to be worth US$2.56 million in 2054, we can backsolve what today’s value of the land needs to be in US dollars, given the higher property tax burden:

The answer is US$518,800.

So, in effect, owning a US$518,000 block of land today is the same as owning a $900,000 block of land in Australia. This 16% discount is purely due to US property taxes being so much higher than council rates in Australia, despite a large stamp duty paid on day 1.

That is the analysis on values. But what a property is worth is one thing, how much people are willing to pay is another.

Impact on willingness to pay

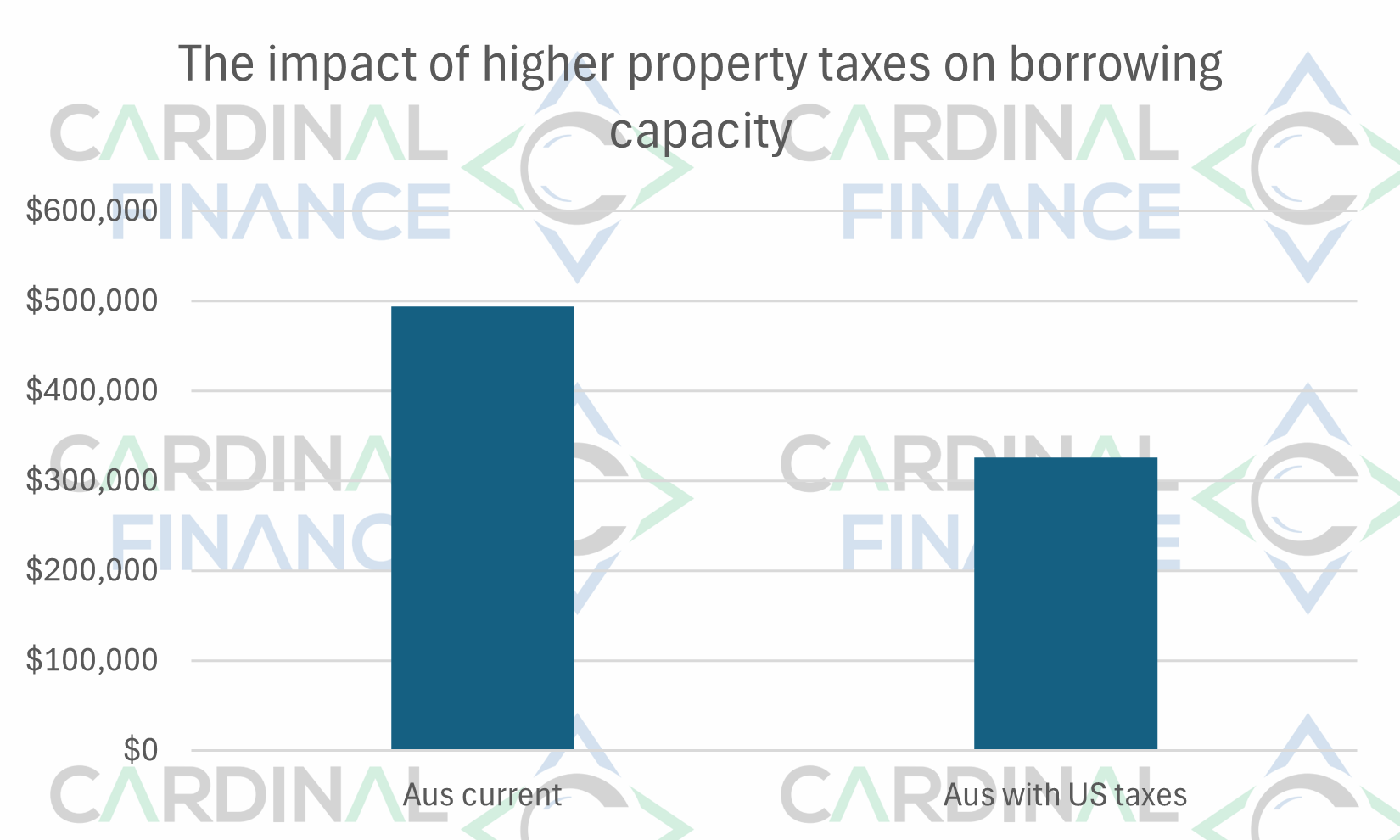

Just imagine buying a new home in Sydney for $1.2 million and expecting to pay council rates of $14,000 a year, instead of $2,000? Assuming all else remains the same, how much would you be willing to pay for that home? How much would the bank lend you?

Circling back to Invitation homes, it paid $4,640 a year in property taxes, with new homes costing it $380,000. That is a tax rate of ~1.2% a year. Imagine your council charging you 1.2% on your $1.2 million home? That would be $14,400 a year. After this, federal income tax and household expenses, how much would a bank lend a median income household in Australia? 34% less.

Property taxes — be careful what you wish for

Politicians and policymakers have tried scrapping stamp duty and replacing it with property taxes. The temptation of scrapping stamp duty and replacing with an annual tax would appeal to home buyers, speculators and developers. It might seem palatable for some, but how would it impact land values over the long term?

This post shows how property taxes can impact land values, but more importantly, borrowing capacity. This would permanently impair property prices in Australia. Something the banks, property owners and eventually Governments will rue.

What do you think? Comment below.